Oil Market 2024: Economic Trends, OPEC+ Moves, and Beyond

From Global Slowdown to Geopolitical Tensions: Navigating the Complexities of Oil Demand and Supply | That's TradingNEWS

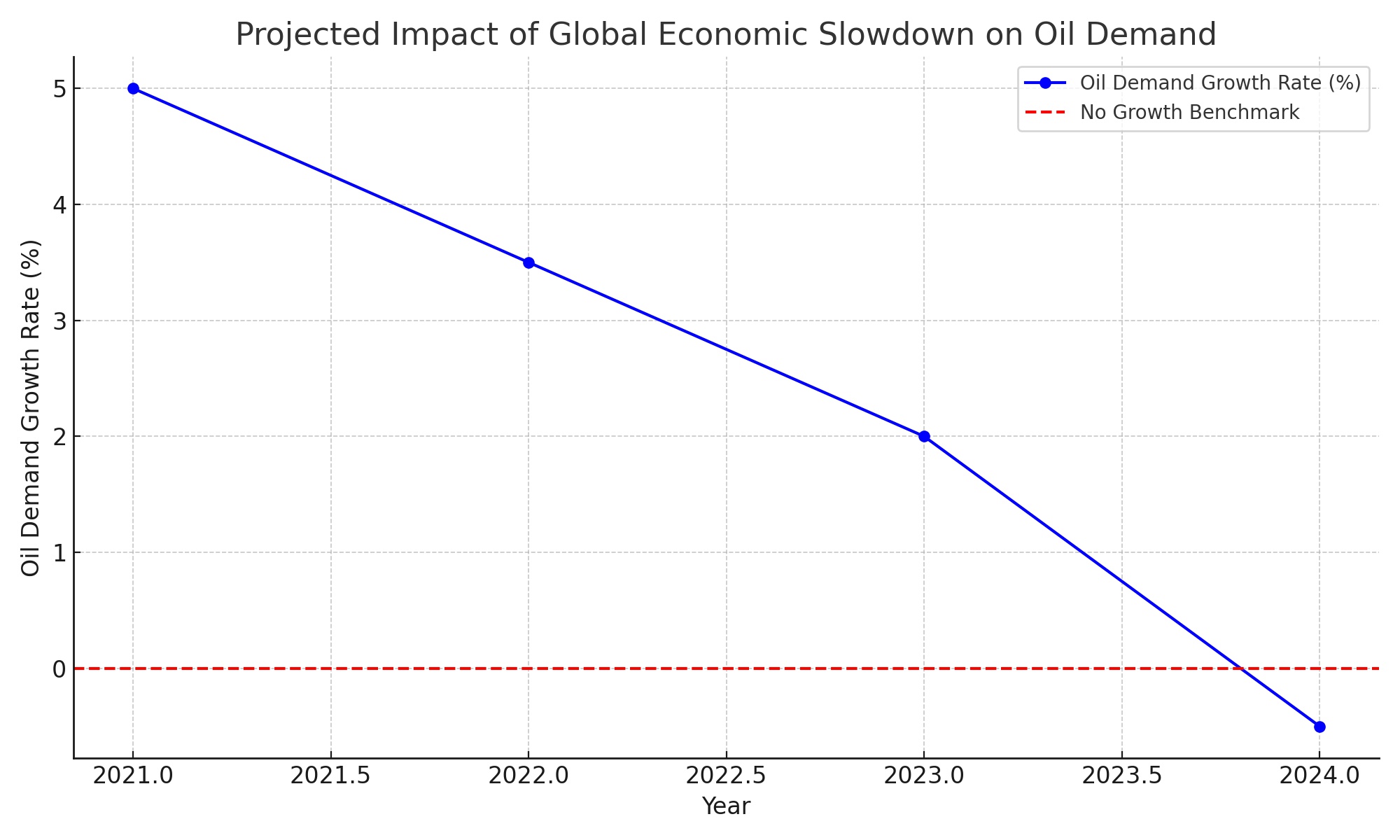

Global Economic Slowdown and Oil Demand

The shadow of a global economic slowdown looms large over 2024, with major economies grappling with the specter of recession. This economic deceleration is expected to dampen crude demand, particularly from China, which has historically been a linchpin in global oil consumption. The anticipation of lessened demand from the world's second-largest oil consumer is a pivotal factor contributing to the expectation of stable or potentially declining oil prices.

OPEC+ Strategy and Its Implications

In 2023, OPEC+ (the Organization of the Petroleum Exporting Countries and its allies), which commands a significant 40% of global oil supply, made a decisive move by announcing additional production cuts totaling 1.65 million barrels per day (mbpd). This was on top of the previously agreed cuts of 2 mbpd from October 2022, cumulatively representing about 3% of global oil demand. These strategic cuts were aimed at bolstering oil prices, a goal that was temporarily achieved as markets responded positively, leading to a price rally.

Saudi Arabia's further voluntary cut of 1 mbpd underscored the group's commitment to market stability. This concerted effort by OPEC+ members not only highlights their pivotal role in global oil markets but also sets the stage for a delicate balancing act in 2024, as they navigate the challenges of economic headwinds and fluctuating demand.

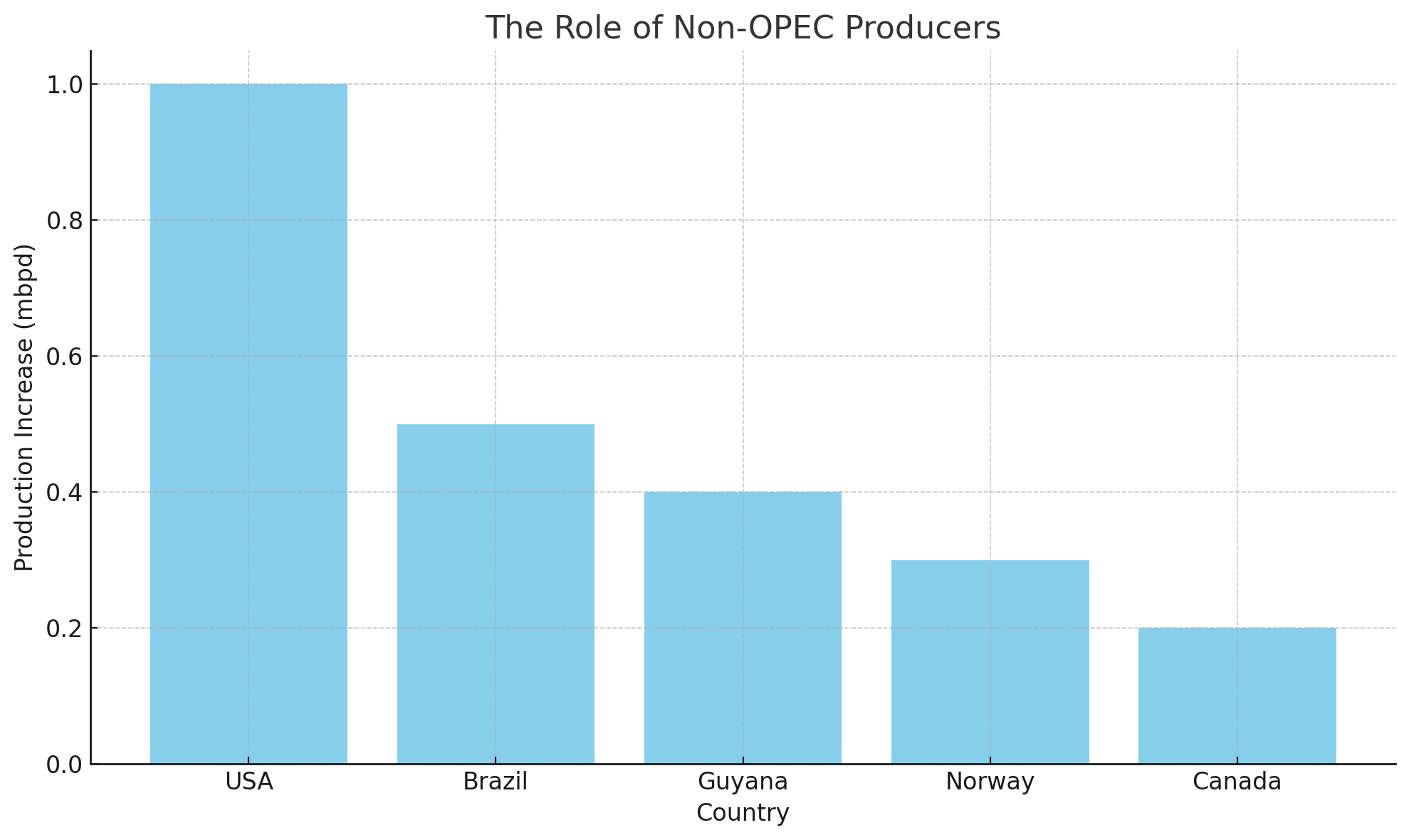

The Role of Non-OPEC Producers

The narrative of oil supply in 2024 is not solely dictated by OPEC+. Non-OPEC producers, notably the United States, Brazil, Guyana, Norway, and Canada, are expected to contribute significantly to global supply. The U.S., in particular, reached a production milestone of 13.24 mbpd, underscoring its growing influence in the oil market. This influx from non-OPEC countries is instrumental in shaping the supply dynamics and could act as a counterbalance to OPEC+'s production cuts.

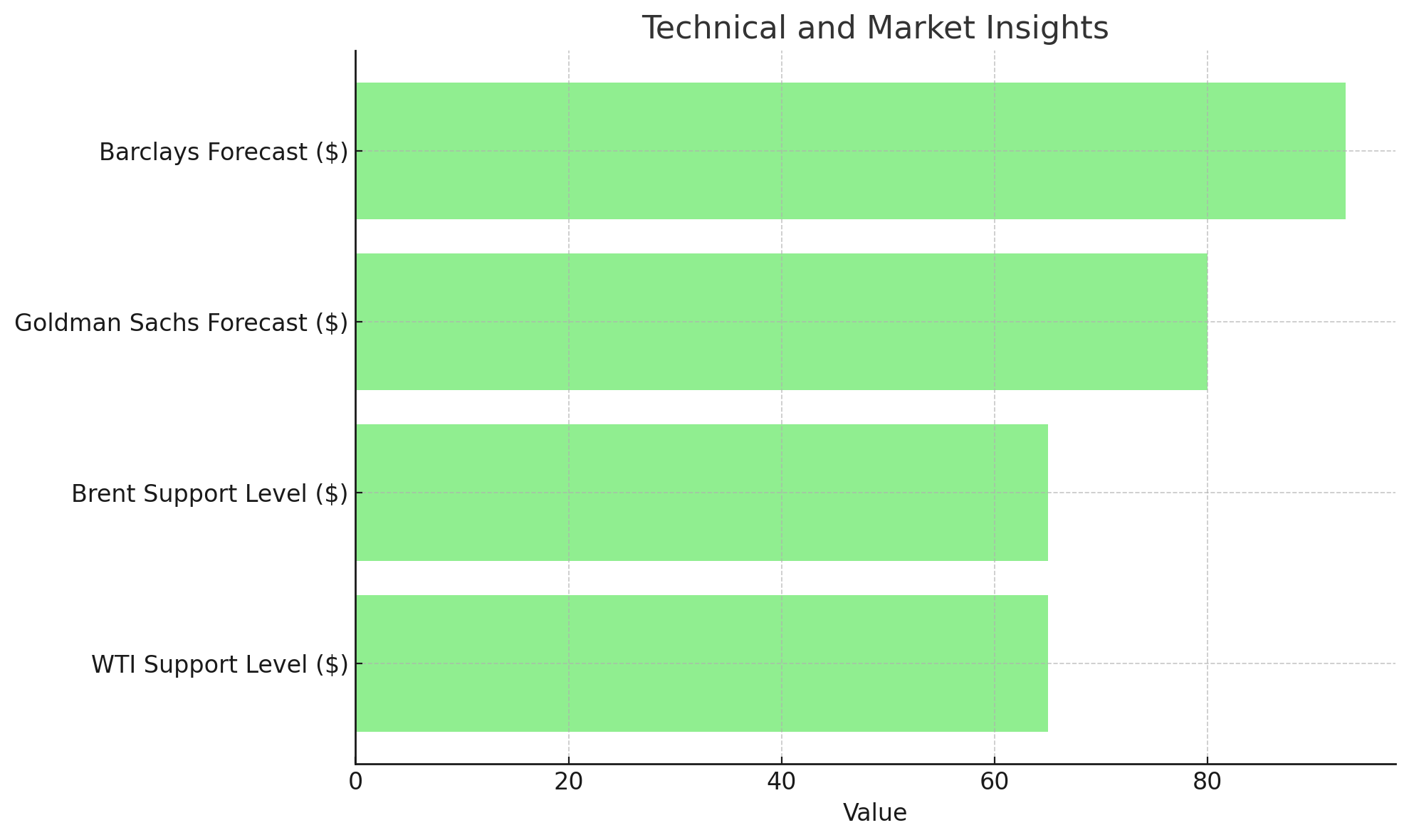

Technical and Market Insights

Technical analysis offers a granular view of the market's direction, with significant support levels identified at $65 for WTI and the mid-$60 range for Brent crude. These support levels suggest a floor for prices, especially if the anticipated global recession materializes. Expert forecasts, including those from Goldman Sachs and Barclays, present a spectrum of expectations, with average Brent prices predicted to range from $80 to $93 in 2024. These forecasts reflect the underlying uncertainties and the complex interplay of supply-demand dynamics, geopolitical tensions, and economic indicators.

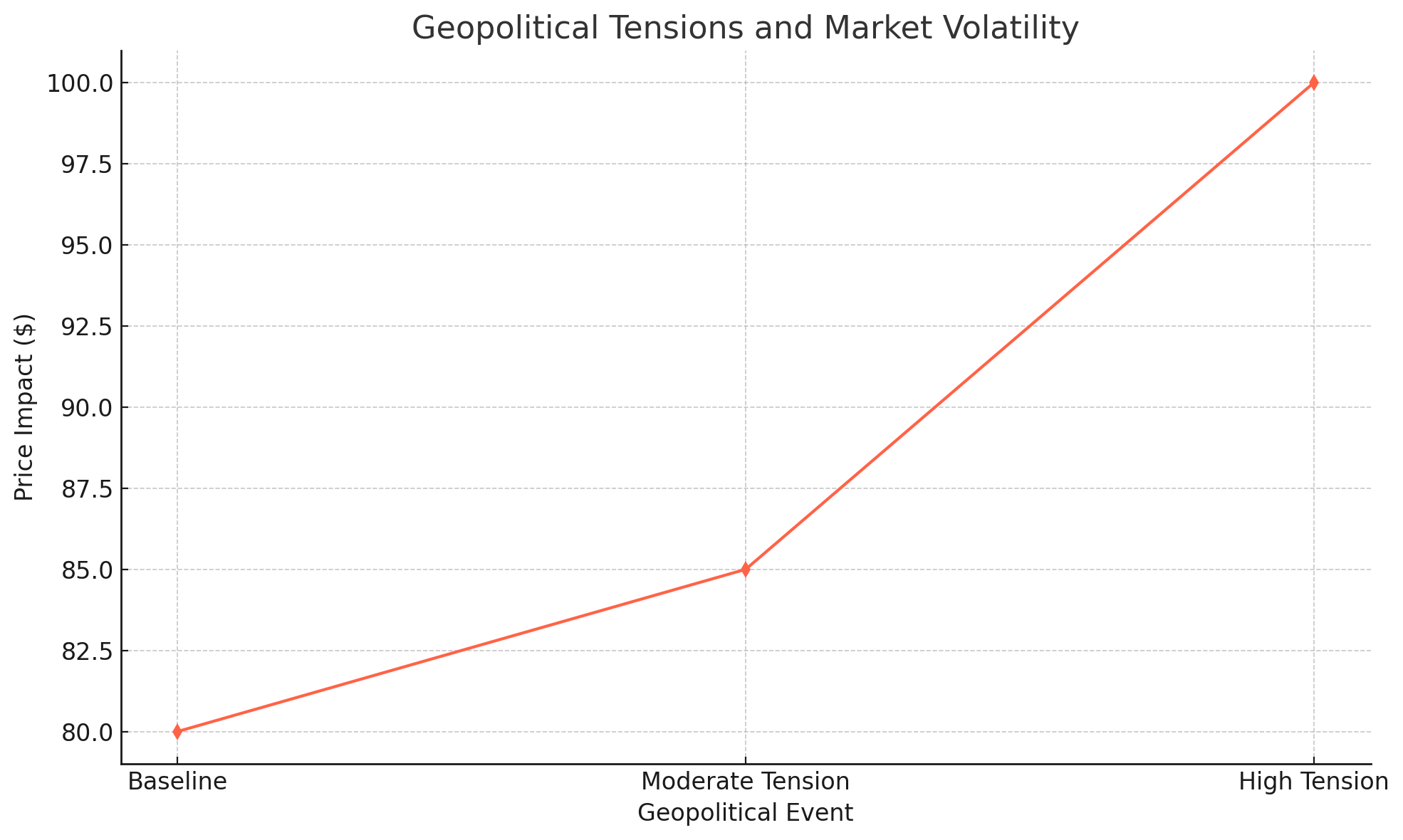

Geopolitical Tensions and Market Volatility

Geopolitical events, particularly in the Middle East, continue to inject volatility into oil markets. The ongoing conflict and tensions not only have direct implications for regional production but also affect global market sentiment, potentially leading to price spikes or increased market volatility. The situation underscores the inextricable link between geopolitics and oil markets, where developments in one sphere can rapidly influence the other.

Consumer Impact and Future Outlook

For consumers, the broader implications of these dynamics are profound. Oil prices influence a myriad of economic sectors, from transportation to manufacturing, affecting prices of goods and overall inflation. The expectation of stable to lower oil prices in 2024 offers a glimmer of hope for consumers, potentially easing inflationary pressures and contributing to a more favorable economic environment.

In conclusion, the oil market in 2024 presents a complex tapestry woven from economic indicators, OPEC+ strategies, non-OPEC production dynamics, geopolitical tensions, and technical analysis. While cautious optimism may be warranted, the interplay of these factors necessitates vigilant monitoring and analysis to navigate the uncertainties ahead. As we move through 2024, the ability of key players to adapt to these evolving dynamics will be paramount in shaping the global oil landscape.

Read More

-

QQQI ETF: A 14.62% Distribution Rate Against a 0.09% SEC Yield as the Call Overlay Caps a 9% Nasdaq Rebound

05.08.2026 · TradingNEWS ArchiveStocks

-

XRP ETF: 7 Funds Add 192M Tokens in 10 Weeks as Assets Fall to $1B and July Inflows Collapse to $27.29M

05.08.2026 · TradingNEWS ArchiveCrypto

-

Henry Hub Holds $2.69 as a 185 Bcf Surplus and Record 112 Bcf/d Production Cap Every Heat Rally

05.08.2026 · TradingNEWS ArchiveCommodities

-

Dollar Holds 157.61 as a $58.97B Joint Intervention Breaks the Yen's Slide From 163.73

05.08.2026 · TradingNEWS ArchiveForex